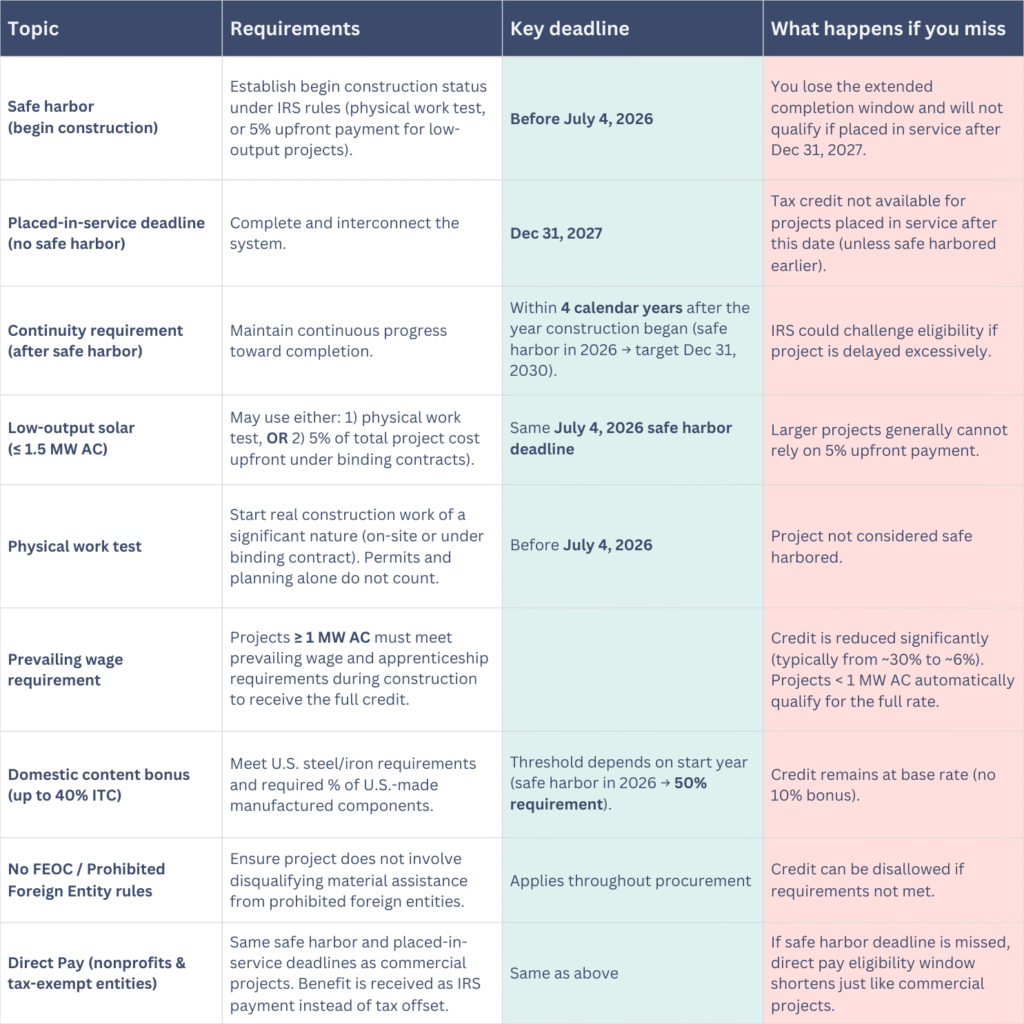

To qualify for the federal clean electricity investment tax credit under the One Big Beautiful Bill Act, most solar projects must begin construction by July 4, 2026—and meet new continuity and foreign-entity restrictions.

The OBBB law accelerated the timeline for commercial solar tax credits. In plain terms:

- If you safe harbor your project on time, you keep a longer window to complete construction and place it in service.

- If you miss the safe harbor deadline you’ll have far less time to finish the project and qualify.

PPM Solar can help you document “begin construction,” structure procurement correctly, and avoid common compliance pitfalls.

Request an OBBB Tax Credit Qualification Review

We’ll confirm which path applies (physical work vs. 5% for low-output), key dates, and the documentation you’ll need.

The two deadlines that now matter most

A) Safe harbor deadline

To qualify under the OBBB rules, you generally must begin construction before July 4, 2026.

B) Placed-in-service cutoff

For most commercial solar projects, the tax credit is not available if the system is placed in service after December 31, 2027 — unless the project safe-harbored earlier under the rules described on this page.

Direct pay for nonprofits

If your organization is a nonprofit, municipality, school, hospital, church, or other tax-exempt entity, you may qualify for direct pay (also called elective payment).

Instead of using the tax credit to offset taxes, eligible nonprofits receive the full credit amount as a direct payment from the IRS.

The safe harbor deadline and placed-in-service timelines are the same as for taxable commercial projects.

If your organization misses the safe harbor deadline, the window to qualify for direct pay becomes significantly shorter — just like for commercial entities.

How you prove “begin construction” (this is your safe harbor)

For most commercial solar projects physical work test is the only method

Except for a specific low-output category (below), the IRS guidance makes the physical work test the sole way to establish that construction began on time.

What it means:

- You must start physical work of a significant nature (on-site or off-site under a binding written contract).

- The test focuses on the nature of the work, not a specific % of spend.

- Preliminary activities (planning, financing, permitting) do not count by themselves.

Exception: low-output solar can still use the 5% safe harbor

If your solar facility is a “low output solar facility” you may establish begin-construction either by:

- Starting real construction work, or

- Locking in at least 5% of the project cost upfront under binding contracts

Low-output definition:

- Must be ≤ 1.5 MW maximum net output (AC).

“Safe harbored” doesn’t mean “pause it” — you must maintain continuity

Beginning construction isn’t a one-and-done checkbox. The IRS requires you to maintain a continuity requirement (a continuous program of construction).

The simple “continuity safe harbor” rule

You are deemed to satisfy continuity if you place the project in service by the end of the calendar year that is no more than 4 calendar years after the year construction began.

If you begin construction by July 2026, the 4-year continuity safe harbor generally lands on December 31, 2030.

New “No FEOC / Prohibited Foreign Entity” restrictions

OBBB added new restrictions that can make a project ineligible if it involves material assistance from a Prohibited Foreign Entity (PFE) (and related restrictions).

Key takeaway for owners:

- This is not just “where panels come from.” It’s a formal IRS eligibility test tied to “material assistance” rules and documentation/safe harbors.

- Treasury/IRS issued guidance in Notice 2026-15, including interim safe harbors and example calculations.

Practical implication: If your project is starting construction in 2026, you should plan procurement and vendor certifications early so your tax credit position isn’t jeopardized late in the build.

Bonus ITC: how 30% can become 40%

If your project qualifies for the full ITC rate (including meeting prevailing wage/apprenticeship where required), the domestic content bonus can increase the ITC by +10 percentage points (often described as “30% → 40%”).

What “domestic content” generally requires

Domestic content is a two-part test:

- Steel / iron manufacturing processes in the U.S. (for structural construction materials), and

- Manufactured products must meet an Adjusted Percentage Rule (a required share of costs attributable to U.S.-made manufactured products/components).

For most solar projects, the commonly used adjusted-percentage schedule is:

- 50% for projects that start construction in 2026

- 55% for projects that start construction in 2027

So if you’re targeting begin construction by July 2026, the domestic content threshold you’ll usually be planning around is 50%.

Quick qualification checklist

Step 1 — Confirm your begin-construction path

- > 1.5 MW (or not “low output”): physical work test only

- ≤ 1.5 MW low-output solar: start real construction or lock in at least 5% of project cost upfront

- Review and approve your contractor’s proposal, including the system sizing, pricing, and ROI

- Confirm utility interconnection requirements

Step 2 — Lock the deadline

- Execute the construction agreement

- Pay the deposit

- Begin construction (5%+ financial commitment for low-output projects) before July 4, 2026

- Begin the engineering and interconnection process

Step 3 — Protect continuity

- Maintain a continuous program of construction

- Target in-service within the 4-year continuity safe harbor window

- Complete engineering and apply for permitting

Step 4 — Validate “No PFE material assistance” risk

- Build procurement plan + documentation aligned with IRS guidance (Notice 2026-15)

- Have manufacturer’s reliance letters/statements on hand for the product ordered

Step 5 — If targeting 40% ITC, plan domestic content early

- Verify the cost/benefit analysis (often, it costs more than 10% to obtain bonus domestic content)

- Confirm the applicable adjusted-percentage threshold for your start year (50% in 2026)

Step 6 — If you are a nonprofit or tax-exempt entity

- Confirm eligibility for direct pay (elective payment)

- Ensure safe harbor and continuity deadlines are met (same timeline as commercial projects)

- Coordinate with your CPA on direct pay filing requirements

Disclaimer: This page is provided for general informational purposes only and does not constitute tax, legal, or accounting advice. Tax credit eligibility depends on project-specific facts and IRS guidance. Always consult your tax advisor/CPA and legal counsel regarding your specific situation.

FAQ section

Does spending 5% automatically safe-harbor my commercial solar project?

Not anymore in most cases. IRS guidance generally removed the 5% safe harbor for wind/solar begin-construction determinations, except for “low output solar facilities.”

What counts as “physical work of a significant nature”?

It’s work that is truly part of building the facility (on-site or off-site under a binding contract). Permitting, financing, and planning alone don’t qualify.

If we begin construction in 2026, do we really have time until 2030?

The IRS continuity safe harbor is 4 calendar years after the year construction began—so yes, projects beginning in 2026 commonly target Dec 31, 2030 for continuity-safe-harbor treatment.

What does “PFE / FEOC” mean for my solar project?

OBBB added restrictions tied to “material assistance from a prohibited foreign entity.” Treasury/IRS guidance (Notice 2026-15) explains interim safe harbors and how eligibility is evaluated.If your organization misses the Safe Harbor deadline, the window to qualify for Direct Pay becomes significantly shorter — just like for commercial entities.